Featured

Table of Contents

Overall personal bankruptcy filings rose 11 percent, with boosts in both business and non-business personal bankruptcies, in the twelve-month duration ending Dec. 31, 2025. According to statistics released by the Administrative Workplace of the U.S. Courts, yearly bankruptcy filings amounted to 574,314 in the year ending December 2025, compared to 517,308 cases in the previous year.

31, 2025. Non-business personal bankruptcy filings rose 11.2 percent to 549,577, compared to 494,201 in December 2024. Personal bankruptcy amounts to for the previous 12 months are reported four times yearly. For more than a years, overall filings fell progressively, from a high of nearly 1.6 million in September 2010 to a low of 380,634 in June 2022.

202423,107494,201517,308202318,926434,064452,990202213,481374,240387,721202114,347399,269413,616 2024310,6318,884216197,2442023261,2777,456139183,9562022225,4554,918169157,0872021288,3274,836276120,002 Extra statistics released today include: Service and non-business bankruptcy filings for the 12-month duration ending Dec. 31, 2025 (Table F-2, 12-Month), A contrast of 12-month information ending December 2024 and December 2025 (Table F), Filings for the most current 3 months, (Table F-2, 3 Month); and filings by month (Table F-2, October, November, December), Personal bankruptcy filings by county (Table F-5A). For more on bankruptcy and its chapters, see the list below resources:.

As we enter 2026, the insolvency landscape is prepared for to move in ways that will substantially impact lenders this year. After years of post-pandemic unpredictability, filings are climbing gradually, and economic pressures continue to affect customer habits. Throughout a current Ask a Pro webinar, our specialists, Investor Milos Gvozdenovic and Attorney Garry Masterson, weighed in on what loan providers need to expect in the coming year.

Legal Protections Under the FDCPA in 2026

The most prominent trend for 2026 is a continual increase in bankruptcy filings. While filings have actually not reached pre-COVID levels, month-over-month growth recommends we're on track to surpass them soon.

While chapter 13 filings continue to heighten, chapter 7 filings, the most typical type of customer personal bankruptcy, are anticipated to dominate court dockets., interest rates remain high, and borrowing costs continue to climb.

Indicators such as consumers utilizing "buy now, pay later on" for groceries and surrendering just recently purchased automobiles demonstrate monetary tension. As a financial institution, you might see more repossessions and automobile surrenders in the coming months and year. You should likewise get ready for increased delinquency rates on vehicle loans and home loans. It's also crucial to closely keep an eye on credit portfolios as debt levels remain high.

We predict that the genuine effect will hit in 2027, when these foreclosures move to conclusion and trigger personal bankruptcy filings. Increasing property taxes and homeowners' insurance coverage costs are currently pushing novice lawbreakers into monetary distress. How can creditors stay one step ahead of mortgage-related personal bankruptcy filings? Your team needs to finish a thorough review of foreclosure processes, procedures and timelines.

Legitimate State Programs for Financial Relief

Numerous impending defaults might arise from previously strong credit sections. In the last few years, credit reporting in insolvency cases has actually turned into one of the most controversial subjects. This year will be no various. But it is essential that lenders persevere. If a debtor does not reaffirm a loan, you ought to not continue reporting the account as active.

Resume regular reporting only after a reaffirmation arrangement is signed and filed. For Chapter 13 cases, follow the strategy terms thoroughly and consult compliance teams on reporting obligations.

Another pattern to see is the boost in pro se filingscases submitted without attorney representation. These cases typically develop procedural problems for lenders. Some debtors might fail to properly reveal their assets, income and expenditures. They can even miss out on key court hearings. Once again, these issues add intricacy to insolvency cases.

Some recent college graduates may manage responsibilities and turn to personal bankruptcy to handle overall financial obligation. The takeaway: Lenders need to get ready for more complex case management and consider proactive outreach to customers dealing with substantial financial pressure. Lien perfection stays a significant compliance threat. The failure to best a lien within 30 days of loan origination can lead to a financial institution being dealt with as unsecured in insolvency.

Consider protective procedures such as UCC filings when delays happen. The personal bankruptcy landscape in 2026 will continue to be formed by financial unpredictability, regulative analysis and progressing customer habits.

Benefits and Risks of Debt Settlement in 2026

By expecting the trends pointed out above, you can mitigate exposure and keep functional resilience in the year ahead. This blog is not a solicitation for company, and it is not meant to make up legal advice on particular matters, develop an attorney-client relationship or be lawfully binding in any method.

With a quarter of this century behind us, we enter 2026 with hope and optimism for the brand-new year., the company is talking about a $1.25 billion debtor-in-possession funding bundle with creditors. Included to this is the general international slowdown in luxury sales, which might be key factors for a prospective Chapter 11 filing.

Preventing Foreclosure Through HUD Counseling17, 2025. Yahoo Financing reports GameStop's core business continues to struggle. The company's $821 million in net income was down 4.5% year-over-year, driven by a 12% decline in hardware and a 27% decline in software sales. According to Seeking Alpha, an essential element the company's consistent income decrease and diminished sales was last year's undesirable climate condition.

Analyzing Chapter 7 and Credit Counseling for 2026

Swimming pool Publication reports the business's 1-to-20 reverse stock split in the Fall of 2025 was both to guarantee the Nasdaq's minimum bid rate requirement to keep the company's listing and let financiers understand management was taking active procedures to resolve monetary standing. It is uncertain whether these efforts by management and a better weather condition environment for 2026 will assist prevent a restructuring.

, the odds of distress is over 50%.

{kind=link}

Latest Posts

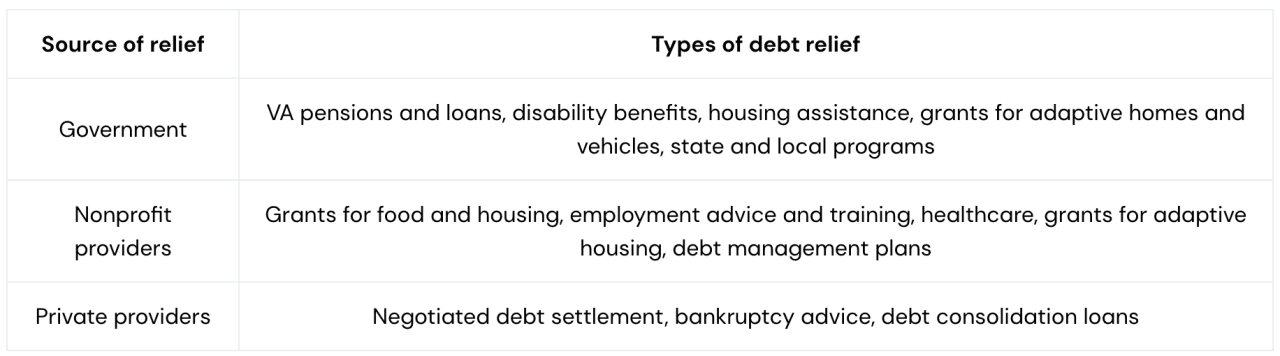

Applying for Government Debt Relief Programs in 2026

Qualifying for Government Debt Relief Assistance in 2026

Steps to Petition for Chapter 7 in 2026